Providing Resources for Claim Audit, Excess Loss Audit and Self-Funded Plan Administration Since 1995. Put Trilogy’s Expertise and Experience to Work for Your Organization.

We publish The Trilogy Claims Administrative Handbook and provide claim audit and consulting services to private corporations, insurance companies, managing general underwriters, Taft-Hartley plans and government municipalities.

Excess Loss Audit Services

Click below for a comprehensive list of our excess loss audit services.

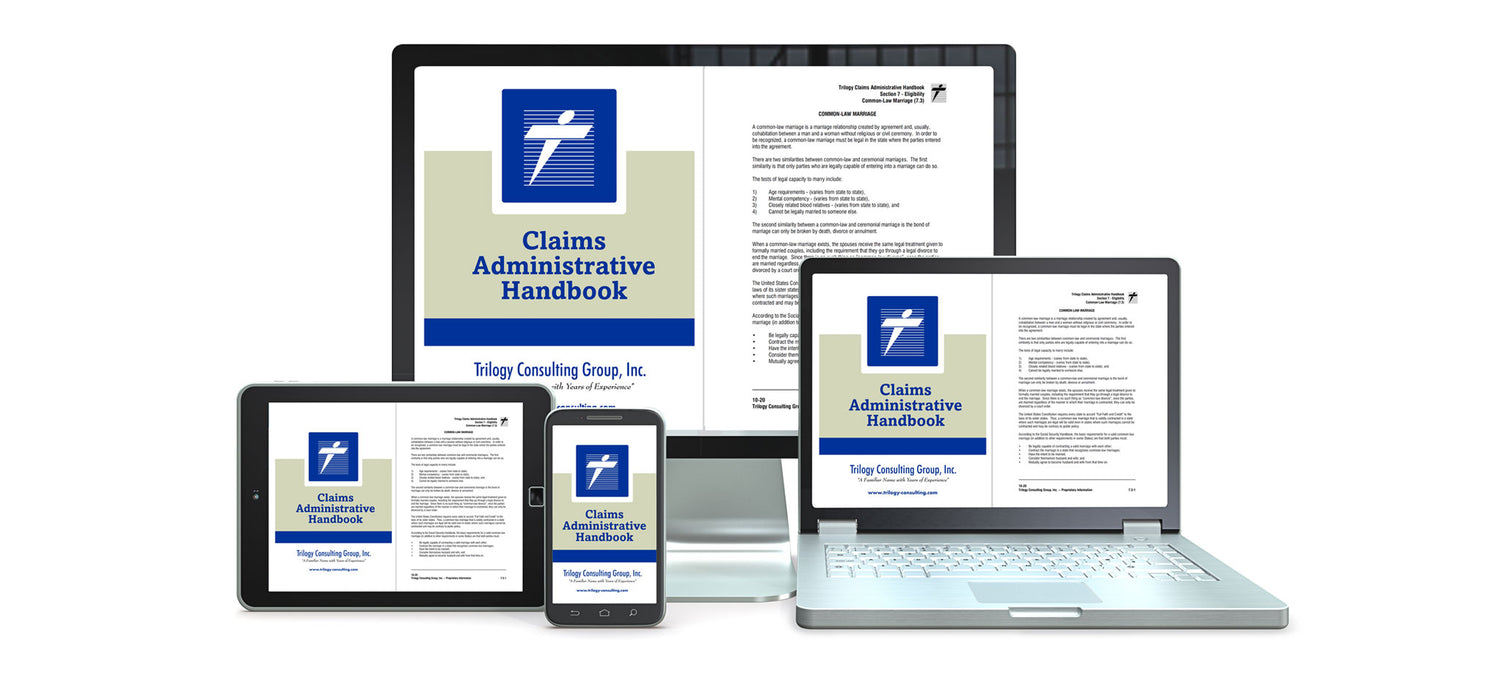

Trilogy Claims Administrative Handbook

The most comprehensive Claims Administration Guide available today.